Stewardship Code Annual Report & SRD II

Polunin Capital Partners Limited — UK Stewardship Code 2026

Disclosures for asset owners and asset managers

A. Describe your organisation, your investment beliefs, your clients or beneficiaries and how that informs your approach to stewardship

Polunin Capital Partners Limited (‘PCPL’, ‘the Firm’, or ‘Polunin Capital Partners’) manages assets for a range of institutional clients including pension funds, endowments and commingled investment funds. The Firm has since inception specialised in investing in Global Emerging Markets for professional/institutional clients, but in 2025 its product offering expanded to include a new International Value strategy, covering Developed Markets ex-USA and Canada. The new strategy commenced with a separately managed account from an existing client; however this client does not permit the Firm to vote proxies, and therefore given that a core element of stewardship is denied by this, these assets have not been included in the following report. Consequently during the year, the Firm’s activities covered by the Stewardship Code were limited to investments in Emerging Market and Frontier Market equity securities. Investments in UK and European equity securities (which derive the majority of their revenues from, or have significant investments in, Emerging or Frontier Markets) formed a small part of the Firm’s investment universe.

PCPL manages assets for a range of professional clients (and fund investors) including pension funds, endowments, and comingled investment funds. Below is a breakdown of our clients/fund investors by geography and type as at 31 December 2025:

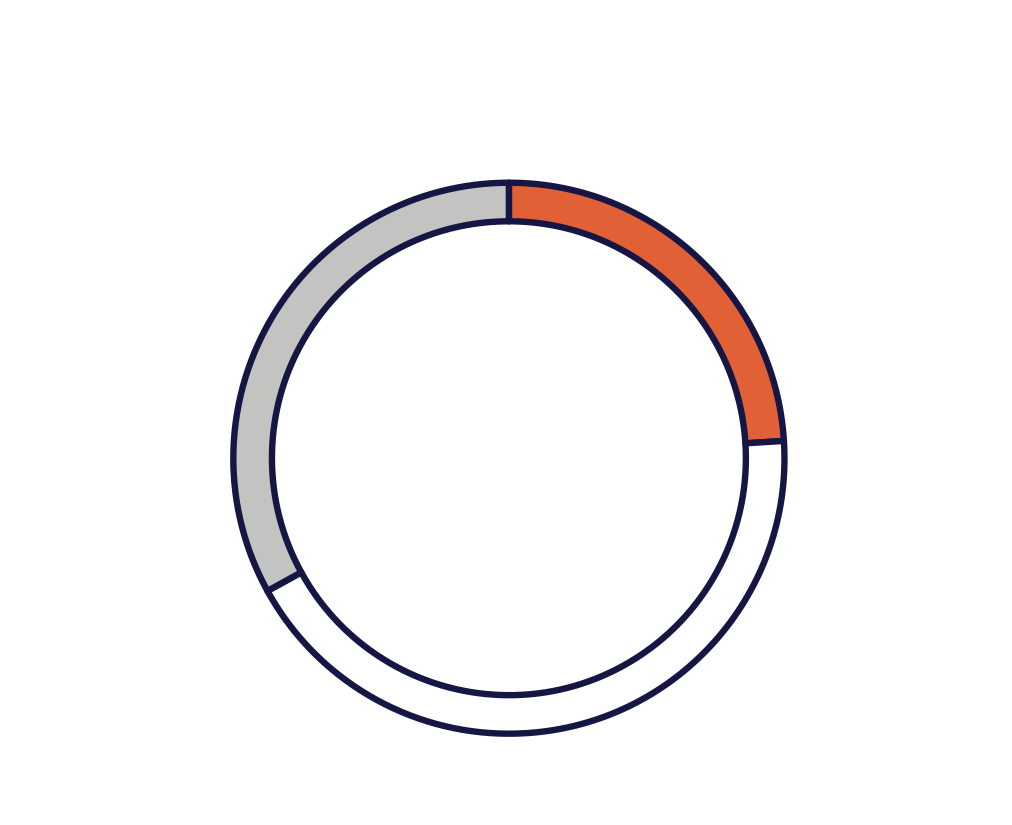

Our client base is predominantly US focused (86%), but we also have significant investment from institutions in Singapore (9%) and Saudi Arabia (3%). We are more diversified in terms of institutional client type with investment managers, public pensions and sovereign wealth representing 52% of our total assets under management (‘AUM’). Endowments, inter-governmental organizations and foundations are the primary source of the remaining balance, representing a further 29% of our AUM. PCPL’s invested AUM is typically over 99% in Emerging Markets listed equities. The chart below shows the geographic split of our AUM as of December 2025:

All the Firm’s investment strategies are underpinned by a common, deep-value investment methodology and process, which is best suited to a longer-term investment horizon (3 to 5 years). The deep-value philosophy is aligned with our stated goal to maximise investment returns by mitigating relevant ESG risks through engagement with investee companies over multiple years, a process that requires investment analysts to engage regularly with the companies they are responsible for. Our deep-value investment style tends to have a higher weighting toward hard-to-abate sectors, and Emerging Markets companies often contend with national energy policies that do not always align with the energy transition expectations of investors from developed markets. Our engagement with investees often involves educating them on investor expectations, and urging them to implement a reporting roadmap alongside improving governance and oversight on sustainability risks. The decarbonisation difficulty in Emerging Markets is generally well understood by clients, but portfolio risks need to be well-managed, and since 2022 we have published carbon emissions and climate risks data of our holdings in the annual Taskforce on Climate-related Financial Disclosures (‘TCFD’) report. Continued engagement with companies on climate risks forms an important part of the stewardship approach.

Purpose

The Firm’s guiding principle is to maximise the long-term economic value of clients’ holdings, using a proprietary replacement value methodology that has been successfully applied and refined over decades and through various cycles. As stewards of clients’ capital and as long-term investors, the sustainability of investees’ business models can be important to investment considerations, as issues such as climate change, resource constraints, diversity, and gender equality create risks and opportunities in our investment universe. Incorporating Environmental, Social and Governance (‘ESG’) criteria into our bottom-up investment process enables us to make better risk-adjusted investment decisions.

Culture

As an employee-owned firm, we emphasise long-term group equity ownership, which is aligned with performance-based remuneration, with robust compliance and risk-management frameworks, to deliver long-term positive outcomes for clients, stakeholders, and our business.

PCPL aims to foster an inclusive environment where employees are engaged and participate in driving the Firm’s strategic objectives. All employees are responsible for upholding the highest standard of integrity, trust and transparency being paramount to clients and stakeholders alike.

Strategy

PCPL believes responsible investment can make a significant contribution to our ability to meet our fiduciary duty to our clients, who expect us to maximise the returns on their investments. Issues such as equality, sustainable development, and climate change affect not only societies, but potentially the long-

term performance of companies, and outcomes for financial assets. The Firm’s philosophy is to focus on direct engagement with a view to affecting operational changes that result in improvements to ESG factors that in turn will act as positive catalysts to share price performance.

In 2019 we established our first ESG policy, and ESG Committee. We began standardising ESG due diligence on an individual strategy basis, with our core strategies utilising in-house ESG scoring, covering a comprehensive range of ESG issues -from climate change to human rights and diversity, which are mapped to the United Nations Sustainable Development Goals (‘UN SDGs’) and are incorporated into investment analysis and active ownership when they are material. We seek to assess the current and future ESG risks and opportunities of a company, and how they affect a company’s potential to reach fair value.

We became a signatory of the United Nations-supported Principles for Responsible Investment (‘UNPRI’) in Dec 2020, and fully revised our Responsible Investment, Climate Change, Proxy Voting, and Exclusion Policies in early 2021, to demonstrate our commitment to investing responsibly.

We monitor the progress of and continue to improve our ESG and Stewardship processes. For example, following our first UNPRI assessment, we began to publish our proxy voting on a quarterly basis, and in 2022 we published our first TCFD report.

In 2023 we fully revised our engagement approach to set targeted objectives on our investees, designed to improve the sustainability outcomes of companies over 4 years.

In early 2024 we joined Spring, UNPRI’s stewardship initiative, to learn more about standards and methodologies in biodiversity to enable us to more effectively engage with investee companies in respect of these issues.

We are mindful of the risk that investment ‘style drift’ can arise from pursuing a too prescriptive, exclusion-based application of stewardship principles, which is why we have adopted a methodology focused on engaging with investee companies to effect changes and improved transparency to safeguard the long-term economic value of our portfolio holdings. We believe that this approach best serves the interests of our clients, who are mainly well-informed institutional investors; the client feedback we have received on our engagement approach has been broadly supportive.

B. Describe how your resources enable effective stewardship

ESG & Stewardship governance structure

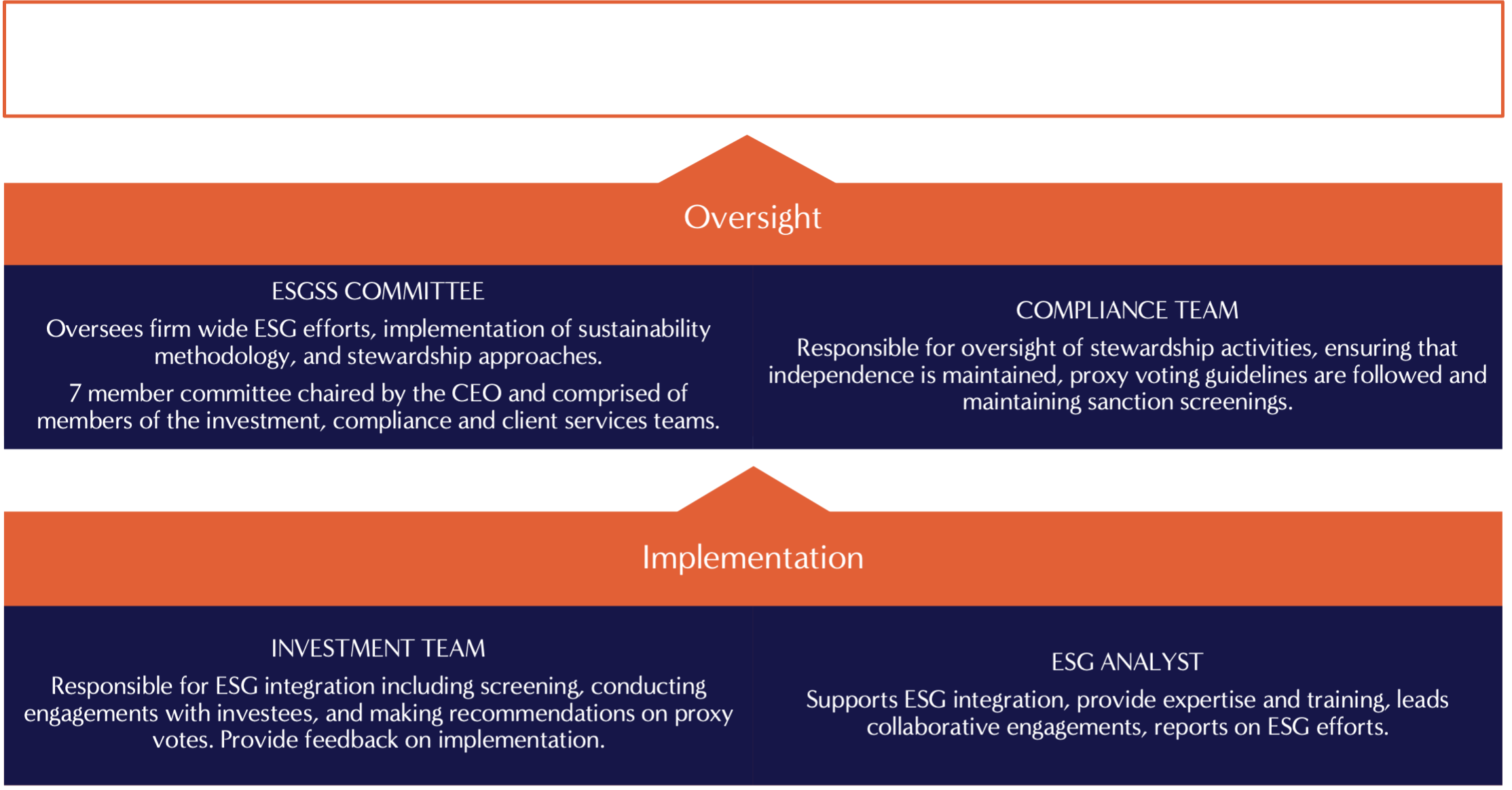

The PCPL Board of Directors has oversight of the company’s strategy and investment objectives and has ultimate responsibility for ESG integration into the investment process and portfolio construction.

Our responsible investment methodology, policy and reporting are overseen by the ESG Committee, which is chaired by our CIO, with membership drawn from our investment, compliance and client service teams. The ESG Committee oversees the development of our responsible investment policy and the methodology for implementing ESG processes within core investment processes. The ESG Committee meets at least quarterly.

Our 15 investment professionals groupwide are responsible for the ESG scoring of their sector and company coverage, for making proxy voting recommendations, and for leading engagement with companies. Our lead analysts have a deep understanding of the regulatory, cultural and competitive backdrop of the countries and sectors our investees operate in, and this knowledge forms an important part of gaining rapport with investees in engagement activities.

Within our investment team there is a nominated ESG analyst, who has achieved the CFA Certificate in ESG Investing. The ESG analyst supports our CIO in the continued integration of ESG into the management of our portfolios, drawing upon their expertise and knowledge, keeping abreast of new ESG developments and policies, and delivering ongoing ESG training in-house as required.

The Compliance team is responsible for oversight of stewardship activities, ensuring that independence is maintained, and proxy voting guidelines are followed. Compliance monitors and ensures that investment processes and products comply with regulations and investment management agreements.

We use ISS databases to support pre-investment checks for breaches of norms, and controversial weapons exclusions. Our internal ESG checklist analyses portfolio companies on their ESG preparedness based on eight sustainability outcome objectives, plus other company specific issues, and pertinent sectoral concerns. Our research is based on publicly available information such as annual reports, annual sustainability reports, news articles, regulatory disclosures, and risks identified by the Reprisk dataset. We combine the checklist with the Reprisk rating (reflecting controversy risk exposure) and Refinitiv ESG scoring (a quality measure) to prioritise investees for engagement, and to identify key engagement topics. The sector investment analyst files written reports on the annual ESG review, and adhoc event-driven engagement.

Whilst Glass Lewis provides the Firm with proxy voting recommendations, and we often refer to their historical recommendations on governance-related engagements, our investment team performs its own assessment of the facts before determining how to vote a particular proxy.

Climate-related datasets from ISS are used in assessing portfolio climate impact and carbon emission exposures, in particular for TCFD reporting.

The Firm’s analysts use Artificial Intelligence (‘AI’) to improve productivity in investment research process, however results generated by AI are reviewed and verified by analysts for relevance and accuracy. We have not integrated AI or AI agents into any area of the Firm’s business. The use of AI is governed by the PCP Artificial Intelligence (AI) Policy, and PCPL’s Written Information Security Policy (‘WISP’) lays out the governance and measures taken related to information and cyber security. We are also a signatory to the AI Company Data Initiative (‘AICDI’), which maps its framework against emerging AI regulations, and conducts annual survey of companies on governance and responsible use of AI, which we expect will help inform the development of our policies on AI.

PCPL’s remuneration policy aims to align compensation with the interests of clients and long-term performance of the Firm. Each individual’s performance assessment includes consideration of their compliance with internal policies and procedures, including ESG policies and procedures, alongside their contribution to the strategic objectives of the Company.

With our Emerging Markets focus it is advantageous for us to employ a highly diverse workforce, including many from the emerging market countries in which we invest, to properly execute our investment process. Across the Polunin group out of 29 employees and 2 independent contractors, a very wide range of nationalities are represented and mostly from developing countries. In response to our Firm’s 2025 Polunin group annual diversity survey, over 44% of staff identified as racially or ethnically Asian, just under 7% identified as Latino, and just over 10% identified as having mixed or multiple ethnic or racial groups. Approximately 27% of our staff identified as female, with a third of working directors and 18% of senior management identifying as female in response to our 2025 survey. We offer flexible working opportunities, which we feel enable us to attract a wider range of applicants to the Firm. Prospective employees are interviewed by a series of different staff before an offer is made, ensuring diversity in the selection panel. Most of the Firm’s future growth in staffing is anticipated to be within our investment team where the benefits to the investment process of ethnic diversity have been self-evident to the Board for many years. Diversity — including skills, experience, ethnicity and gender — is just as important at Board level.

Through our ESG Committee meetings we continually assess the effectiveness of our governance structures and processes, and review whether internal requirements and client expectations are being met. We have Board level commitment to ensure that sufficient resources are deployed in support of our ongoing ESG and stewardship initiatives, from headcount to third party ESG data purchases from third party specialist ESG data providers.

C. Describe your stewardship policies and processes, and how you review them.

PCPL’s long-term investment horizon, typically 3 to 5 years, is intertwined with our approach to stewardship, looking to enhance investor’s value through engagement with our portfolio holdings to minimise reputational and sustainability risks. Our approach, policies and reporting are overseen by the ESG Committee, chaired by our CIO, and reporting to our Board of Directors which ensures the implementation of responsible investment at the Firm, this includes the review and approval of all related policies and procedures or updates to existing documents.

The Firm’s ESG Committee meets formally on at least a quarterly basis, meeting more frequently or on an ad-hoc basis as needed. This ensures that the business can be responsive to outcomes from norms-based and exclusionary screening. Engagement with companies on ESG and proxy voting matters, including collaborative efforts with other investors, are also discussed at the meetings.

The ESG Committee membership includes portfolio managers alongside representatives of the compliance, and client services teams. It regularly invites guest attendees to report to the Committee and lend specialist insights, and also to promote the Firmwide understanding of ESG goals and objectives.

The Firm’s stewardship policies are reviewed annually by the ESG Committee and approved by the Compliance team, to ensure that they are fair and balanced, and that best practices and up-to-date climate guidelines are adhered to. Our responsible investment and ESG policies are published on our website at https://polunin.co.uk/#responsibility.

We aim to ensure that our stewardship reporting is fair, balanced and understandable. Quarterly proxy voting reports and annual engagement reports are written in plain English, and are subject to review and approval by the ESG Committee, with our annual TCFD report additionally reviewed by the Board and signed off by the CEO. Once approved they are reviewed by our Compliance team before being published on our website, and are available to all members of the public. Since 2024 our engagements have focused on progress on the specific objectives and outcomes set for target companies.

PCPL is a small firm and as such does not maintain an Internal Audit department. Instead we engage external auditors, experts and consultants to ensure that our compliance framework is subject to regular independent assessment; and our governance and operational structure is subject to a full systems and controls audit. The Firm does not use external assurance to evaluate its ESG policies and processes, but we continue to assess the most appropriate method for assuring the effectiveness of our stewardship activities. During 2025 we did not identify any gaps in our stewardship practice.

D. Describe how you manage stewardship-related conflicts of interest to put the best interests of clients and beneficiaries first.

The Polunin group is a privately owned enterprise, with the majority of staff owning an equity interest, and in which the original founders and majority shareholders are actively involved in day-to-day management. PCPL recognises the importance of managing potential conflicts of interest on behalf of its clients when voting their shares and engaging with investee companies. PCPL will consider all potential conflicts of interest that identifies, or which are brought to its attention, and will determine if a material conflict of interest exists. Our principal objectives when considering matters such as engagement and voting are always to act in the best interests of our clients and to treat them fairly.

The Firm’s Compliance team and Board are responsible for implementing systems and controls designed to review potential and actual conflicts of interest on a quarterly basis. Conflicts can arise in situations when the Firm:

- is likely to make a financial gain, or avoid a loss, at the expense of a client (including the funds managed by the Firm and their investors);

- has an interest in the outcome of a transaction conducted on behalf of a client, distinct from the client’s interest in that outcome;

- has incentive to favour the interests of one client over another;

- conducts the same business as the client; or

- receives or will receive an inducement from a person other than the client in relation to services provided to the client in the form of monetary or non-monetary benefits or services.

Policies and procedures relating to conflicts of interest are available on the Firm’s website (https://polunin.co.uk/conflicts-of-interest-policy/ ). If a potential conflict is identified, business functions will be segregated to maintain independence and to prevent the identified conflict from crystallising. This may include information barriers, separating functions and adding supervision, or reassigning functions altogether.

All staff members receive compliance training and are required to attest quarterly to Compliance that they understand the Firm’s conflicts of interest policy, including disclosing any personal conflicts such as their personal trading activities, the receipt of gifts, benefits or entertainment and outside business interests.

The Firm has an order aggregation and allocation policy which governs the management of buy and sell orders across accounts sharing the same investment strategy, aiming to ensure fairness to clients through consistency in transaction prices and equitable allocation of part-dealt orders. The policy’s implementation and adherence to it is overseen by the Firm’s Operations and Compliance teams.

The ESG Committee comprises staff members from the broad range of departments at the Firm, and includes the CEO who is also the Chief Investment Officer. The structure of the Committee ensures broad involvement in policymaking and is designed to engender the consistent dissemination and implementation of policies and procedures throughout the organisation, aiming to minimise the risk of conflicting activities occurring.

Staff members are required to obtain prior approval from Compliance before engaging in any employment outside of their employment with the Firm. Staff members are also required to obtain approval from Compliance prior to taking an interest or accepting an appointment in any outside business, and in particular before becoming a director, an officer or adviser to a company, charity, or any other entity, whether it is a paid position.

PCPL commenced securities lending activities for certain clients in the first quarter of 2025. Arrangements were structured to ensure that all client revenue (net of bank securities lending agency fees) will be retained by the relevant accounts. PCPL as investment manager is remunerated through its management and performance fees and does not charge any additional fees or recharge costs to our clients in respect of securities lending.

The review of conflicts of interest is dynamic, with the Compliance team raising any perceived or potential issues with senior management at the Firm whenever they arise, and as a standing item at the Firm’s regular quarterly Board meetings.

The Compliance team retains control over the submission of proxy votes, to ensure that voting intentions do not come into conflict with the Firm’s proxy voting policies, and that voting is consistent across all clients. Where the Firm is permitted to vote on behalf of client mandates, it has full discretion to do so; meaning that the potential for client voting instructions to come into conflict with the Firm’s voting policies is very unlikely to arise. During the calendar year 2025 reporting period, the Firm has not identified any actual conflicts of interest in connection with its stewardship or engagement activities.

Potential conflict case study 1: Chief Investment Officer’s personal holding in one of the Firm’s investment products.

How it would be addressed: We continue to monitor and manage carefully any potential conflicts of interest arising from senior management and client investors’ overlapping investment. Aside from measures to mitigate the risk of single-person bias in trading and investment activity, any potential conflicts with other shareholders on proxy voting matters are mitigated by the Compliance team having oversight of exercising the proxy voting.

Potential conflict case study 2: An analyst or fund manager is made an insider in the course of discussion with a company.

How it would be addressed: The Firm’s Restricted List is updated to include the company name, and the reason for a trading restriction being imposed. Pre-trade restrictions are added to the trade management systems and personal account dealing register to ensure no trading in the name is possible. The Compliance team will seek confirmation from the analyst or fund manager that the suspected material non-public information is no longer an issue (i.e. it has entered the public domain before removing the trading restrictions. In 2025, there were no representations made to add a company name to the Restricted List which remained empty during the year.

E. Describe how you maintain a dialogue with clients and/or beneficiaries

Our client services team meet with our clients regularly in performance reviews and due diligence meetings, answering any ESG and stewardship-related queries that may arise. Clients generally receive monthly updates on portfolio performance and attributions, with a more detailed quarterly or semi-annual report with portfolio manager commentary. Voting activity is reported on a quarterly basis via our website, and we engage with investees on controversial votes and proposals where we have concerns where timing allows, with rationale of our voting decision disclosed publicly. Our stewardship reporting is publicly available, and segregated mandates may request and receive customised stewardship reporting specific to their portfolios.

2025 Activities and Outcomes Report

Principle 1: Signatories integrate stewardship and investment to deliver long-term sustainable value for their clients and beneficiaries

Our core asset class is listed equities, comprising approximately 99% of invested AUM, and it is important to note that our approach to the integration of stewardship through engagement does not differ across our clients, asset classes or geographies.

The resourcing of ESG analysis (monitoring through holding and exiting) and engagement (monitoring through holding and exiting) is managed within the investment team directly; we do not have a separate sustainability research team. Our analysts are responsible for analysis of all risks including both financial and ESG risks, and performing relevant further engagement of investees. This approach is the same across all geographies within our investment universe. We ask analysts to focus on:

- Companies’ environmental and social policies, processes and disclosures, focusing on material risks of particular sectors, e.g. water use in the semiconductor industry, human rights in the construction industry;

- Whether past controversies have been addressed through improvement in processes; and

- Companies’ governance structure and historical track record.

Whilst we have developed our own methodology to analyse companies on ESG matters, we also purchase external research to monitor ESG-related controversies. This includes both normative issues such as human and labour rights, and involvement in controversial weapons, and forms part of the screening process prior to investment. Companies with a verified failure to respect established norms are excluded for investment purposes.1 Existing investees undergoing remediation or that have alleged failures are prioritised for engagement. During calendar year 2025 we did not have any investees with alleged breaches.

Issues identified during the internal scoring process form the basis of the engagement discussion with investees. In addition, the process of producing periodic ESG reporting to clients, and filling in requests for proposals, provides feedback on clients’ focus topics in sustainability. From these sources, we have identified the following eight sustainability outcome objectives:

- Start publicly reporting on environmental impact such as greenhouse gas (‘GHG’) emissions, water usage, and waste generation;

- Set targets on reduction of the above, in particular absolute GHG emission over 2026-35, and report on progress;

- Report on and commit to mitigating processes for physical climate risks;

- Introduce board-level oversight of sustainability risk management;

- Disclose diversity and inclusion data at different seniority levels;

- Introduce time-bound targets and measures to improve diversity and inclusion performance;

- Achieve greater levels of board and senior management level diversity over time;

- Report annually on labour and human rights due diligence to identify, prevent, and mitigate risks at the company, as well as at the suppliers and contractors levels.

We believe the above topics will become more material to investors over time, and therefore it is paramount that investees have policies in place and improve disclosure on such matters. Furthermore, it is our belief that weakness noted in respect of a company’s ability to deliver against the eight sustainability outcome objectives above could foretell an increased risk of controversies, so the engagement process with companies acts as part of our risk management process.

1 We reserve the right to amend the scope of screening and exclusion based on internal verification and analysis.

Regarding climate engagement, we are a supporter of TCFD, a signatory of UNPRI and a participant of Climate Action 100+ (‘CA100+’).

As an investor signatory to Workforce Disclosure Initiative (‘WDI’) – an annual survey and collaborative engagement programme to provide data on workforce practices, run by Thomson Reuters Foundation – we have gained practical insights on how to identify and address workforce issues, a pressing but under- addressed area in Emerging Markets.

Although our proxy voting is mostly related to governance issues, such as board composition, remuneration, and corporate actions that may disadvantage minority investors, we have encouraged our team to engage prior to voting on significant items, and investees have found the feedback and suggestions helpful. With more systematic record keeping of engagement, tracking and reviewing historical voting records on proxy voting platform, we have had more active dialogue with investees on our views on governance, diversity and climate.

Principle 2: Signatories identify and respond to market-wide and systemic risks to promote a well-functioning financial system

PCPL’s investment methodology is bottom-up and focused on the fundamental value of a company using industry valuation techniques. There is no formal integration of macro-economic and geopolitical analysis in this process. However, as the valuation comparison of companies across Emerging Markets uses the US Dollar as a common currency, macro risks and events are identified and often can be captured through changes in FX rates and their effect on the relative valuation. By example, a company’s valuation relative to its peers will become more expensive if its local currency strengthens appreciably against the US Dollar (which will in turn be a function of top-down economic or political factors). This is captured by our proprietary database on a timely basis.

Political or social instability, or diplomatic developments could affect investment in certain countries. There are varying levels of government supervision and regulation of exchanges, financial institutions and issuers across countries. In addition, the way foreign investors may invest in securities in certain countries, as well as limitations on such investments, may increase the volatility and risk of loss to investments. As these risks develop, they are identified by our investment analysts, who have deep knowledge and expertise in emerging markets countries, through their ongoing fundamental value analysis and by keeping abreast of local and international news and announcements. At certain parts of the cycle, our analysts may monitor policy and political developments, with scenario analysis.

Managing geopolitical risks: the unleashing of Trump tariffs set the volatile backdrop for EM investors in 2025. However as the year progressed, prior consensus on safe heavens, re-shoring, and industrial controls started to shift, and dispersion between markets with attractive valuation and economies better positioned to absorb geopolitical shocks, and expensive but less resilient markets, widened. While we continue to monitor geopolitical tensions, our investment approach has been consistent throughout.

Managing sustainability risks: Emerging Markets typically have greater exposure to sustainability risks than developed markets. Listed companies in Emerging Markets are often subject to less extensive sustainability-related reporting requirements making it challenging for the Firm and external providers to identify and assess the materiality of inherent sustainability risks. The assessment of sustainability risks of investees is carried out on an annual basis, the results of which are summarised and reviewed by the ESG Committee, to integrate into the investment decision-making, and monitor potential or actual material risk to long-term risk-adjusted returns. We summarise sustainability risks in our investment universe as follows:

- Climate change management is at an early stage in Emerging Markets, most countries are at the beginning of establishing targets and action plans to reduce environmental impact, and government implementation and enforcement of policies to limit climate impacts are often lacking or non-existent. Climate impacts may include greenhouse gas emissions and climate change, water stress, biodiversity and deforestation, emissions and waste both toxic and non-hazardous, and environmental management in the supply chain.

- Countries in Emerging Markets often lag developed markets in respect of labour and human rights practices, child labour, equal opportunity and pay, freedom of association, sexual harassment, occupational health and safety, code of ethics and conduct, confidentiality for whistle-blowers, antibribery and corruption, and supplier monitoring in respect of the aforementioned practices. There can be gaps in consumer rights and protection, including product quality assurances, prevention of misselling, monitoring inappropriate online content and behaviour, and consumer data protection, privacy and cybersecurity.

- Governance risks may be more pronounced in Emerging Markets owing to less developed corporate governance frameworks, and a lack of legal protection or redress for stakeholders and minority shareholders.

Our analysts perform ESG reviews on relevant portfolio companies on an annual basis, this includes reviewing corporate reporting, news items, third party databases, to build an engagement focus list. Please refer to Principle 3 on corporate engagement.

The analysis performed in support of our TCFD reporting has focused our attention on engaging with investee companies to encourage the setting of medium-term emission reduction targets, as the alignment level remains low in Emerging Markets. Given our value-oriented investment style, the portfolio is naturally tilted towards carbon-intensive, hard-to-abate sectors such as materials (chemicals, steel, cement, aluminum), and transportation (aviation, shipping, rail). While we have seen some rapid progress in developing low carbon technologies amongst our investees, we continue to engage with investees on targets that will align with energy transition.

It is worth noting that the quantification of physical climate risks remains a challenge for some of our investees, and also for us at a portfolio level, due to the lack of detailed geospatial data, and difficulty in modelling extreme weather patterns. However, we stress the importance of physical climate risks in our annual sustainability review with investees.

Participation in industry initiatives:

As an investor signatory to WDI, an annual survey and collaborative engagement programme to provide data on workforce practices, we gained practical insights on engaging with investees to manage human and labour rights issues in the supply chain. Since 2022, we have actively encouraged investees to join. In 2025 we engaged a record number of investees, with a total of 14 companies participating. In the 2025 WDI Awards, our investee CPDC was runner up “Best First Time Responder (Core Indicators)”, and Hyundai Department Store won runner up in “Most Improved Overall”. Other winners included both Top Glove and Acer winning runner up in “Most Improved (former core indicator responder)”, with special mention in “Workforce Action” (plus special mention in “Most Transparent” for Acer), Alibaba with special mention in the “Workforce Action” and “Most transparent” categories. Green Cross, HTC, Lens Technology, Ping An Insurance, SK Networks and Samsung E&A all received special mention in the “Most transparent” category.

We also joined PRI’s Spring stewardship initiative on biodiversity in 2024. At the end of 2025 we commenced kick off of the Hankook Tire engagement group, with us as the lead investor.

In the future we will focus our efforts on:

Identifying and managing climate risks, both transition and physical. To increase the proportion of portfolio companies that are climate resilient and transition aligned, we engage annually with relevant companies in respect of their approach to setting interim carbon reduction targets, and the identification of sector-specific physical climate risks.

Sustainability processes and reporting, encouraging companies to improve material sustainability processes, governance, and disclosures, with a particular emphasis on supply chain human and labour rights.

Diversity and inclusion, with those companies where we believe there is a lack of diversity in skills, or balanced representation of views, to introduce measures to improve at board and senior management levels.

Governance best practices, improving independence of board structures, preventing corporate actions that disadvantage minorities.

Principle 3: Signatories engage to maintain or enhance the value of assets

A. Firm Engagement

Engagements with portfolio companies can be summarised as follows:

- Company specific monitoring (bottom up): investment analysts work with portfolio companies to improve how they manage or disclose ESG performance or issues, as identified in the internal, monthly screening processes, or in response to events or queries. Investee companies are prioritised by the level of risk and size of position.

- Strategic engagement priorities (top down): based on the eight sustainability outcomes, we engage with investees on an annual basis, taking into consideration material issues for the valuation of our companies, clients’ focus topics, and market and regulatory developments. The current priorities are carbon reduction target-setting, diversity and inclusion at board and senior management levels, and supply chain labour and human rights monitoring. We identify the companies most exposed to these topics for engagement, prioritising larger positions and larger companies who are more likely to be able to lead change in the sector.

- Proxy voting engagements as the vast majority of proxy voting issues are related to governance within Emerging Market listed equities, this is often the best opportunity to discuss governance structures and diversity and inclusion related matters with companies, prior to voting, and also throughout the year.

Engagement is an important part of the investment process for listed equities, which accounts for over 99% of our invested AUM. Our engagement approach does not currently differ across strategies or geographies. Our investment team carries out engagement activity directly, so we can combine the monitoring of ESG risks with our nuanced understanding of companies’ operations and sector issues. The investment team engages as part of our regular meetings with companies, phone calls, and emails, or by taking part in collaborative engagements. We maintain records of our engagements internally, the progress of which is regularly reviewed by the ESG Committee. If progress has stalled, then matters are escalated.

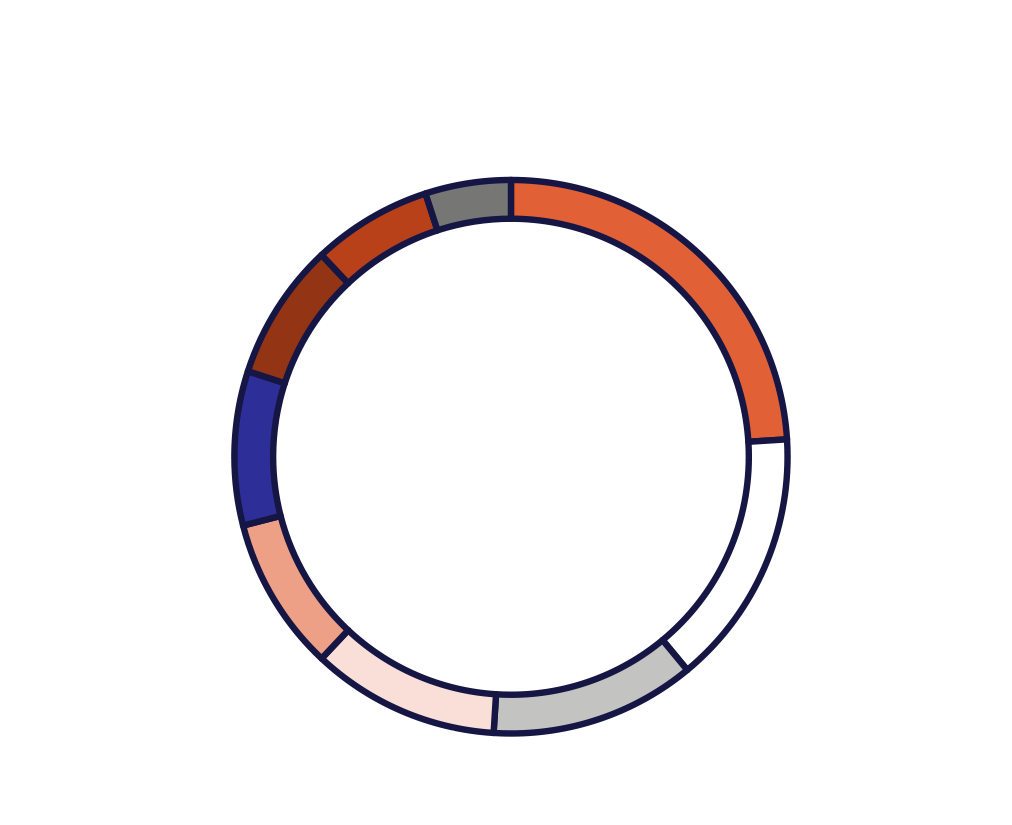

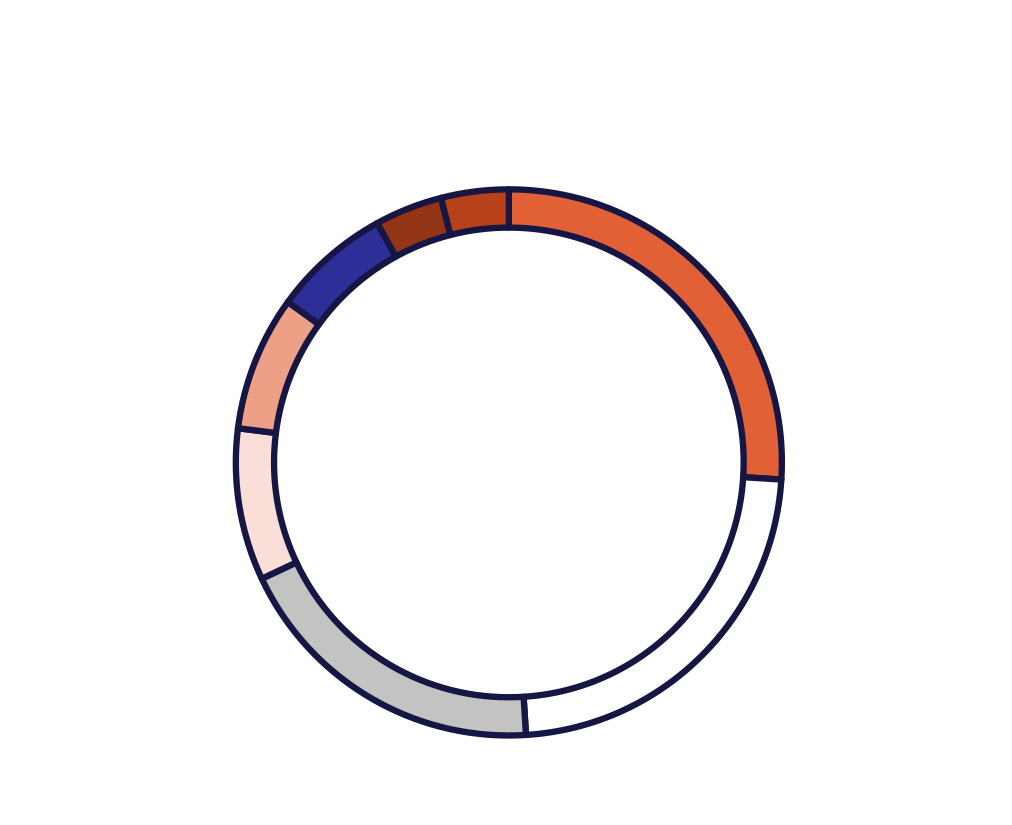

We carried out 96 engagements in 2025, 35 of which were facilitated by external providers in collaborative engagements. 15 engagements were concluded in 2024. Engagement by theme is shown in the following pie chart:

24% of on climate-related risks: setting clear mid-term carbon reduction targets and clarify the method of reduction; better management of sector-specific physical climate risks. Management of biodiversity and deforestation.

43% on social issues: to identify obstacles to improving female participation and retention, in particular at senior management levels, supply chain human and labour rights monitoring.

33% on governance issues: board independence and diversity, capital issuance, related-party transactions, director remuneration, and ESOP.

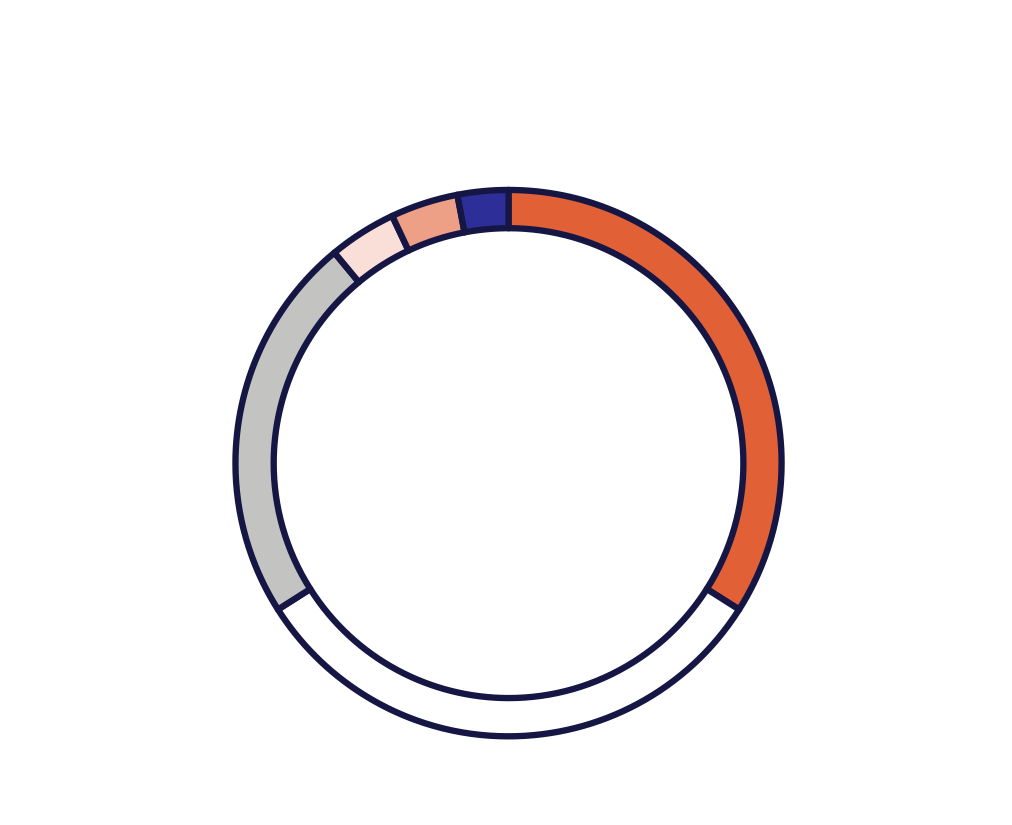

The following show split by sector and country. While this broadly reflects our portfolio exposure, there are more engagements carried out in China and in the IT sector.

Case Study – Sinopec Engineering (‘SEG’, China)

SEG provides integrated refining and petrochemical engineering and construction services to emerging markets customers.

Engagement objectives:

- Set targets on absolute GHG emission over 2026-35, and report on progress;

- Report on and commit to mitigating processes for physical climate risks.

Process:

In 2025, we held two engagements on two key environmental priorities: setting longer-term GHG emissions targets, and strengthening disclosure of physical climate risks.

On emissions targets, we noted that disclosure remained limited, with only a 2021-2025 cumulative intensity-reduction target of 5.7%. We encouraged the company to introduce medium- and long-term targets to provide a clearer roadmap for emissions reduction and demonstrate stronger commitment.

On physical climate risk, we highlighted that, although the 2024 ESG report identified relevant risks, the disclosure lacked sufficient granularity, with hazards such as typhoons, floods, and heavy rainfall grouped together. During our engagements, we encouraged the company to provide more specific and decisionuseful disclosures.

Outcomes:

Following our continued engagement, the company introduced annual targets for 2026-2030 in its latest 2025 ESG report, marking a meaningful improvement from previous disclosure, which only extended to 2025. We continue to encourage the company to set longer-term targets through 2035.

On physical climate risks, the company has since improved disclosure by distinguishing different types of risk, and providing greater detail on timing, affected regions, scope of impact, and financial implications. We look forward to future disclosures on mitigation measures.

The company remains receptive to investor feedback and we expect further improvements on disclosures going forward.

Case Study – Sinopharm (China)

Sinopharm is one of the largest wholesale and retail distributor of pharmaceutical products and medical devices in China.

Engagement objectives:

- Introduce diversity targets at senior levels;

- Improve disclosures of environmental impact across the supply chain.

Process: We have conducted annual engagements with the company over the past three years, focusing on environmental disclosures and board diversity targets. Our initial reviews found that environmental disclosures were minimal — meeting only the baseline regulatory requirements — and that previously stated board diversity targets had been withdrawn.

We communicated our concerns to management and highlighted the benefits of enhanced disclosure transparency and a more inclusive workforce. The company recognised the need for improvement, and responded with enhancements in its 2024 Sustainability Report, which included the first-time disclosure of Scope 3 emissions data, and female representation across management. While no new board-level gender diversity targets were introduced, the company reaffirmed its commitment to maintaining at least 20% female representation on the boards of the company and its subsidiaries.

We acknowledge these steps as positive progress, while noting that further improvement remains. The management confirmed ongoing efforts to strengthen its ESG practices, including pursuing third-party verification of emissions data. The company would consider our recommendation to conduct climate scenario analysis.

Outcomes: Management has recognised the importance of diversity in senior leadership and independent verification of sustainability data. The company has indicated that discussions are underway as part of its 15th Five-Year Plan, which is expected to include new ESG targets and actions for improvements.

Case Study – Dongfang Electric (China)

Dongfang Electric is a top diversified power equipment manufacturer in China.

Engagement objectives:

- Environmental disclosures on emission reduction targets and physical climate risks

- Diversity disclosures and human rights due diligence across the supply chain

Process:

This engagement represented our first formal annual ESG dialogue with Dongfang Electric, building on earlier exchanges in which the company indicated it was developing internal policies and measures aligned with Hong Kong Stock Exchange guidelines. Following our 2025 outreach, the company agreed to a structured engagement covering emissions, diversity, and supply chain management.

Our review of the 2024 ESG report noted progress relative to prior disclosures, including the trial reporting of Scope III volume data and the appointment of one female director to the Board. We shared investor perspectives on disclosures in the following areas:

- Long-term emission reduction targets and physical climate risk assessments to reflect the company’s climate strategy.

- Benchmarking diversity metrics, such as gender pay gap data and time-bound diversity targets.

- Supply chain due diligence on labour and human rights to support risk prevention and mitigation.

Management provided helpful context on their current approach.

As a state-owned enterprise, long-term emission reduction targets are set in alignment with the government’s 15th Five-Year Plan; as an interim step, the company indicated that scenario analysis on carbon reduction pathways through 2030 could be included in next year’s ESG report.

Research on physical climate risks began in 2025, with disclosure planned for the 2027 reporting cycle.

On diversity, management noted industry-specific considerations in setting gender targets and expressed openness to disclosing the median gender pay ratio.

On supply chain management, pre-qualification serves as the primary preventive mechanism, with third-party verification presenting practical challenges, given the scale of the supplier base.

Outcomes:

The engagement marked a constructive step forward, with the company showing greater openness to transparency and receptive to concrete examples that balance disclosure feasibility with investor asks.

Case Study – Samsung Life (South Korea)

Samsung Life is one of the largest life insurers in South Korea, offering life, health, and annuity products.

Engagement objectives:

- Expand emissions reporting boundary and set mid-term reduction targets;

- Achieve greater levels of board and senior management diversity over time;

- Improve and formalise supply chain labour and human rights due diligence;

- Incorporate ESG KPIs into executive compensation.

Process:

Between 2023 and 2025, we conducted three annual ESG reviews with the company, with the following progress:

On the environmental side: (1) Scope 1–2 emissions declined in 2024, after two consecutive years of increases; (2) disclosures were further strengthened through a methodology upgrade to market-based Scope 2 accounting, and an expanded Scope 3 reporting boundary; and (3) a phased renewable energy transition roadmap aligned with RE100 was introduced.

On governance, executive bonuses are now tied to emissions reduction targets set by the board, with renewable transition targets to be incorporated into KPIs from 2026.

On social, the company is conducting human rights impact assessments on a regular basis, and is reviewing the possibility of expanding disclosure in future ESG reports. More work needs to be done with board diversity, as there is still only one female director on the board.

Outcomes:

Meaningful progress has been made on emissions measurement quality and executive ESG accountability. Management expressed willingness to continue improving its ESG practices. Key areas yet to be addressed include the establishment of a mid-term Scope 3 reduction target, board gender diversity, and expanded supply chain disclosure.

Case Study – HTC (Taiwan)

Leading VR/ AR/ XR headset and software brand.

Engagement objectives:

- Start publicly reporting on environmental impact such as greenhouse gas (‘GHG’) emissions, water usage, and waste generation;

- Set targets on reduction of the above, in particular absolute GHG emission over 2026-35, and report on progress;

- Report on and commit to mitigating processes for physical climate risks;

- Introduce board-level oversight of sustainability risk management;

- Disclose diversity and inclusion data at different seniority levels;

- Introduce time-bound targets and measures to improve diversity and inclusion performance;

- Achieve greater levels of board and senior management level diversity over time;

- Report annually on labour and human rights due diligence to identify, prevent, and mitigate risks at the company, as well as at the suppliers and contractors level.

Process: Since 2019, we have engaged with HTC to discuss issues ranging from environmental disclosure, climate risk, to corporate governance, and gender and inclusion disclosures.

1,2,3. Climate: initially HTC did not have Scope 3 disclosures or carbon reduction targets. The company began reporting Scope 3 emissions in 2021, with audit of parent and subsidiaries completed in 2022 and 2023 respectively.

HTC’s SBT commitment was approved in 2023, with a 42% reduction target in 2030 compared to the base year of 2021, and 90% reduction target by 2050 versus the base year.

Prior to 2022, ESG matters were overseen by senior executives. We highlighted the need for board-level sustainability oversight, and to link climate management KPIs to executive performance.

In 2024, HTC published its first TCFD report.

4. Sustainability governance: In 2022, HTC upgraded the former Corporate Social Responsibility (‘CSR’) Committee to the ESG Committee, chaired by Chairwoman Cher Wang, reporting to the Board of Directors on ESG management policies, strategies and execution. The company admitted that the costs of supporting international initiatives were very significant at their current operating scale, and there was a learning curve for the Board to provide guidance and supervision on ESG matters. In our discussions with the Chief Sustainability Officer (‘CSO’) in 2025, certain senior management performance targets linked to ESG KPI will be introduced in 2026.

5,6,7: Diversity: Currently very few employees utilise parental leave, due to the low birth rate (In Taiwan, the mandatory parental leave is up to two years before the child reaches the age of three, employee receives 80% of their salary up to a maximum of 6 months). The company has always been supportive of flexible work options for those with family care needs. The CSO has also mentioned plans to subsidize female employees’ IVF treatments.

8. Supply chain sustainability: the company previously withdrew from Responsible Business Alliance Validated Assessment Program (‘RBA VAP’) due to costs, but had rejoined since 2023. Annual written audits were carried out with suppliers, on-site audits were focused on higher risk suppliers. HTC encouraged suppliers to join RBA VAP, on a voluntary basis, due to the company’s size.

Outcomes: As of December 2025, objectives 1, 2, 5, 8 are met, 3, 4, 6, 7 are work in progress.

B. Collaborative engagement

As a Firm we believe there is strength in numbers when it comes to engaging with our holdings, particularly with larger companies and on sector or policy issues. Collaborative engagement is also useful in those situations where independent escalation has not produced a desirable outcome or during times of significant corporate or economic stress.

The Firm is a signatory to the UNPRI, a participant of the CA100+ and Spring (PRI-led collaborative engagement on biodiversity). We are also a member of the WDI.

The WDI aims to increase transparency around workforce practices by encouraging companies to report data on topics such as decent work and human rights. We have actively engaged with our holdings, as we believe the need for Emerging Markets corporates to align their workforce practices to international standards will only become more pressing over time.

In 2022 our investee Sun Art Retail Group Ltd, a major grocery chain in China with 100,000 employees, became one of the first Chinese participants in WDI. In 2023, COSCO Shipping Ports participated in the WDI, as the first Chinese state-owned enterprise. In 2025 we engaged a record number of investees, with a total of 14 companies participating. In the 2025 WDI Awards, our investee CPDC was runner up “Best First Time Responder (Core Indicators)”, and Hyundai Department Store won runner up in “Most Improved Overall”. Other winners included both Top Glove and Acer winning runner up in “Most Improved (former core indicator responder)”, with special mention in “Workforce Action” (plus special mention in “Most Transparent” for Acer), Alibaba with special mention in the “Workforce Action” and “Most Transparent” categories. Green Cross, HTC, Lens Technology, Ping An Insurance, SK Networks and Samsung E&A all received special mention in the “Most Transparent” category.

Case Study – Ping An Insurance (China)

Ping An is one of the largest diversified financial holding companies in China, operating across insurance, banking, asset management, securities brokerage, and fintech businesses.

Engagement objective:

Invite the company to participate in the Workforce Disclosure Initiative (‘WDI’) survey to improve workforce-related ESG disclosures.

Process:

In 2025, we conducted three engagements with Ping An, including a dedicated conference call with the WDI team, with the aim of encouraging the company to become one of the first Chinese companies in the financial sector to participate in the survey. We also addressed Ping An’s questions and concerns through follow-up emails.

Ping An indicated that capacity constraints from managing multiple concurrent ESG reporting obligations were a barrier to participation. In response, we encouraged the company to begin with submission to the core indicators of the 2025 survey, with a view to expand the scope and depth of disclosure in subsequent years as internal processes mature.

Outcomes:

Ping An participated in the 2025 WDI survey, and management expressed willingness to expand the scope of its disclosure in subsequent years.

C. Escalation

The Firm undertakes a four-year process of engagement, with escalation after 18 months at the latest. This may include public engagement with the board, withholding support on standard governancerelated resolutions (such as director re-elections or approving the reports and accounts) or by filing or co-filing shareholder resolutions. If remediation remains inadequate or ineffective after the engagement process, the Firm will consider whether the residual ESG risk is significant enough to trigger a divestment.

Unless an individual separate account mandate specifies otherwise, the escalation approach is uniform across all of our clients and geographies for our core strategies. However as long-term investors in Emerging Markets equities, we are mindful of cultural sensitivities, and the need for long term cooperation, whilst maintaining independence and avoiding conflict of interest. Escalations may take the form of voting against directors on governance-related resolutions, and in some cases, divestment. We try to find different avenues to engage with companies, through alternative contacts or collaborative platforms, to keep the dialogue alive. However, in cases where there is a significant deterioration in the ESG risk of the company, the position is considered for exclusion or divestment.

Principle 4: Signatories actively exercise their rights and responsibilities

The Firm aims to vote all proxies on behalf of clients that permit it to do so. On request we will discuss with clients the rationale of our decisions when they differ from those of their own proxy advisors. To publicly demonstrate our commitment to stewardship, we publish proxy voting summaries on our website on a quarterly basis. Our proxy voting policy is aligned with our ESG criteria, which is applied to all companies in all funds. We expect our investees to uphold corporate governance standards by:

- creating sustainable, long-term value;

- protecting shareholder rights;

- maintaining integrity in corporate behaviour;

- ensuring an independent and efficient board structure;

- aligning incentive structures and remuneration with long-term interests of shareholders; and

- ensuring accurate, timely and transparent disclosures, whether it is financial, governance, environmental or social.

PCPL uses the Glass Lewis platform to manage and execute our proxy voting. We refer to the proxy advisor’s voting recommendations, but ultimately vote according to our publicly disclosed proxy voting guidelines, and analysts are responsible for reviewing the proxy advisors’ recommendations and may make specific recommendations. However individual country governance codes are often less demanding about board tenures and board diversity. In such cases the lead analyst making recommendations on the vote will take into account the company’s circumstances and general corporate governance track record. The lead analyst is also responsible for analysing and making recommendations on proxies regarding complex transactions and controversial votes, and will engage with the company before or after when possible. Members of the compliance team exercise oversight on the final voting decision.

We coordinate with custodians and our proxy voting service during the account set up process to ensure that ballots for all the shares we are eligible to vote are received in a timely manner. The custodians are linked to our proxy voting service such that ballots reflect up-to-date client/fund stock positions. We monitor any discrepancies which are dealt with by the custodians or ballot distributors.

Some of our funds have participated in stock lending from Q1 2025, and we have established the Securities Recall Policy for Proxy Voting to ensure that securities can be recalled or restricted from being loaned in advance to enable us to exercise material proxy votes. We maintain caps on the proportion of stock holding permitted to be lent, such that we retain a portion of shares in each votable stock to be able to vote.

In 2025, we voted 99% of the eligible 4477 resolutions in 564 meetings, of which 12% were voted either Abstain or Against. In total, we voted Against or Abstain in 540 resolutions, most of which were against Board directors, from low levels of Board independence, exceedingly long tenures for Independent Directors, over-boarding, no audit or remuneration committee independence, or lack of Board diversity. Another frequent reason for lodging Against votes was a lack of rationale being provided by a company when seeking a general mandate for dilutive capital raising, as well as excessive compensation reports where the proposed remuneration plan is found not to be in shareholders’ best interest.

Our proxy voting policy and voting summary, including rationale on Against and Abstain votes, can be found on www.polunin.co.uk/#stewardship

Case Study – Dongfang Electric (China)

Dongfang Electric is a top diversified power equipment manufacturer in China.

In a special meeting in June 2025, the board proposed to make amendments to procedural rules for general

meeting, including the removal of the class shareholder distinction for certain articles.

We voted Against the proposals, reflecting our following concerns:

- Loss of separate class voting rights: Removing the class shareholder distinction would mean

that holders of domestic shares and overseas-listed foreign shares would no longer vote as separate

classes on matters such as share issuances and repurchases. Such resolutions would instead require

only a simple majority of all shareholders. - Increase dilution risk: The removal of class-based distinction used to calculate issuance limits

could result in substantial dilution, especially the existing issuance limit of 20% per class is already

material. - Weaken minority shareholder rights: Eliminating the requirement to hold separate shareholder

class meetings would erode the rights of minority shareholders.

The proposals did not pass at the H share class vote, recording 92.7% and 83.6% Against votes respectively. Combined with our Against vote on the general mandate at the previous EGM, the company has since engaged more proactively with us to better understand the rationale behind our voting decisions.

Case Study – Yunnan Copper (China)

Yunnan Copper is one of major copper smelting company with exposure of upstream copper mining assets in China.

In a special meeting in Aug 2025, the board proposed to acquire 40% of Liangshan Mining which is owned by their parent company through private placement to the parent company.

We voted Against certain aspects of the transaction, primarily relating to issue price discount, valuation and compensation, due to concerns about potential misalignment with minority shareholders’ interests:

- Preferential treatment of major shareholder: The private placement is solely to the controlling shareholder, resulting in potential dilution of approximately 11% to total outstanding shares, at an issue price of around 35% discount. This benefits the controlling shareholder at the expense of minorities who face dilution.

- Concerns over asset valuation: The reappraised asset was three times the original, mainly due to revaluation of mining rights, and the price-to-book multiple of around 4 times is significantly higher than recent comparable transactions.

- Limited performance guarantee: The performance compensation is capped at the total transaction consideration, which in our view provides limited downside protection for the buyer in the event of losses.

The resolutions were nonetheless passed, with more than two-thirds of shareholders voting ‘For’.

Principle 6: Signatories monitor and hold to account stewardship service providers

In tandem with the development of our own ESG methodology to analyse companies, we have continued to purchase external research to monitor ESG related controversies. This includes both normative issues such as human and labour rights, and exposure to controversial areas such as controversial weapons. We also buy in third party data and estimates on carbon emissions. We conduct reviews of our external ESG research providers on an annual basis, to understand changes in methodologies and research focus areas.

In 2025 we discussed with ISS on their controversial weapons methodologies and research process. We also investigated the differences between their climate models and how we could understand the reduction needed for sector alignment.

PCPL procures proxy voting platform services from Glass Lewis. The platform provides enhanced reporting capabilities, access to Glass Lewis’ voting policy recommendations, and the systematic implementation of our voting policy which promotes more consistent decision-making. While we do not vote purely based on purchased recommendation data, the Glass Lewis recommendations are referenced by our analysts. Since the start of the stock lending programme, we have worked with Glass Lewis to understand when ballots are received against the value dates for proxy voting in different markets, to better manage our stock recall process.

We began purchasing ESG risk data from Reprisk in 2023. The provider was selected because its broad coverage aligned well with our Emerging Markets small/mid-cap universe, and because it drew from public sources and stakeholder reports that complimented our own research approach. Having previously provided feedback to Reprisk that their data content was lacking publicly available information in certain languages, we have noticed that additional language capabilities have been added over time.